Introductory Economics

Economics Defined

Economics is the study of the allocation of scarce resources among unlimited human wants.

Unlimited human wants? May have enough of this or that, but will always want more of something, as a society if not as individuals.

Wants vs needs. Difficult to know what a person needs. Wants easy to identify, if you say you want something that is sufficient.

Needs for survival?

Needs to be functional in society?

Needs to be popular in your social setting?

Needs to be well off?

Maslow’s hierarchy of needs…

Resources (in the broadest sense) are scarce in this context, always want more than we have. At any one time, not enough stuff available to satisfy all human wants.

Scarcity – requires that we make choices, more of this or more of that but not both

Macroeconomics/Microeconomics

Macro – big things, the large view of the economy, Total Output, Total Unemployment, Overall Price Levels

How the overall economic system makes allocation decisions.

Micro – small things, a person’s income, the price of gasoline, the sales of one industry or one business.

Deals with how individual persons and individual businesses make decisions about allocation of scarce resources.

What, How and For Whom?

Questions all economic systems must answer

What to produce?

Among all of these unlimited human wants for goods and services, what are we going to produce to satisfy them?

How to produce it?

How are we going to assemble the resources that we have and organize the production of goods and services to satisfy some wants?

Who gets what is produced?

Among all the humans and their unlimited wants, who gets the goods and services that we are going to produce?

What and for whom relatively clear

How refers to the factors of production

Factors of Production

Land (natural resources) Rent

Includes land and natural resources, rent has slightly different meaning here

Labor – human effort Wages

Wages include all returns to labor, wages and salaries

Capital – produced means of production Interest

Capital equipment, buildings and also ideas – organizational schemes

Intellectual capital

Interest has slightly different meaning, not return on money but return on capital investment

Entrepreneurship – innovative management Profit

Not just plain old management, innovative management

WalMart vs other retailers as an example

Opportunity Cost – cost of the alternatives that you give up to pursue some activity

Example, retail store at end of year shows net of $10,000, was it profitable?

Yes in accounting terms

Probably not in economic terms

Applies to all factors, have to consider the alternatives, what you give up if you devote a factor to a particular use

Any good or service can be produced with different mixes of factors of production, trade-offs

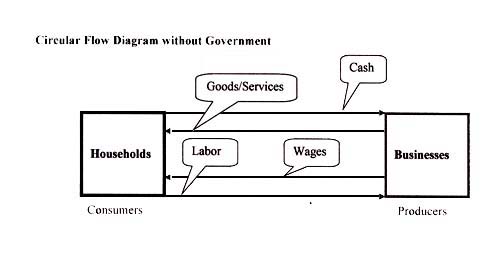

Tradition, Command, Market Systems – Mixed Systems

Three ways to answer the three questions, What? How? For Whom?

Tradition – the way we have always done it. Think of traditional societies.

Command – someone makes the decisions. Think of the Soviet Union or monarchies. Role of government.

Market System – decisions are dispersed throughout system, producers bring goods to market, consumers buy what they want. Think of the farmers’ market.

In practice most systems are mixtures of all three. How is US a mixed system? Tradition, command, market?

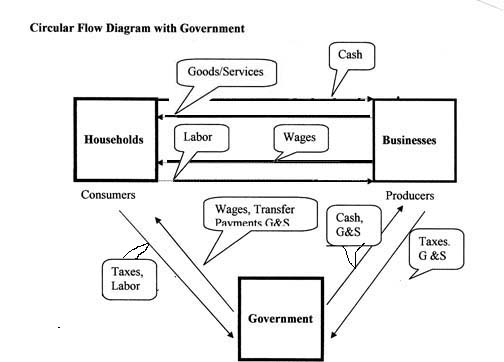

Role of Government is controversial in free market system. What is the appropriate role of gov in the economy?

Role comes about for at least two reasons:

Markets favor efficiency over equity. Powerful incentives for efficient operation – profit motive. Sometimes society wants more equity.

Efficient outcome might result in huge disparities in income and wealth. Is that good?

What does gov’t do to change distribution of wealth and income? Taxes, welfare benefits, social programs

Sometimes markets fail, are not efficient. Gov’t. intervenes to make them more efficient.

Monopoly power – one or a few large businesses dominate a market – can raise prices arbitrarily

What does gov’t do to control monopoly power?

Laws prohibit certain actions, behaviors. Breakup of ATT, law suit against Microsoft.

What share of US economy is from government? Is it too much, too little?

Comparative figures, 2001, % of GDP from Gov.

Sweden 53%

France 49%

Italy 47%

Germany 45%

UK 39%

Japan 38%

Canada 37%

US 29%

S. Korea 23%

Review of graphs

Vertical and horizontal axes

Relationships

Lines and slopes

Curves